💥5% Remittance Tax? U.S. Bill Takes Aim at Indian Diaspora Wallets

A Controversial Tax on Immigrant Remittances

A new U.S. legislative proposal ironically dubbed “The One Big Beautiful Bill” hides a harsh surprise for immigrants and their families abroad. Tucked within this broad tax package is a plan to levy a 5% excise tax on all international money transfers made by non-U.S. citizens. In practical terms, this means an H-1B software engineer or even a green card holder sending money home would lose ₹5 out of every ₹100 sent – a costly skim off the top of hard-earned wages. Proponents argue the tax will raise revenue to make the 2017 tax cuts permanent and fund border security, but experts in cross-border business and immigration are raising red flags. Is this “beautiful” bill a clever way to fund U.S. priorities, or a blunt instrument that burdens immigrant workers and strains international ties? In this article, we dissect the economic and geopolitical rationale of the proposal and its far-reaching implications for the Indian diaspora and U.S.-India business corridors.

The 5% Remittance Tax: Policy Rationale vs. Reality

Under the proposal, a 5% tax would be withheld from any remittance (international money transfer) sent abroad by a non-U.S. citizen, including lawful permanent residents and individuals on work or student visas. U.S. citizens are explicitly exempt. The tax would be collected by banks and transfer services at the point of transaction, effectively charging immigrants extra for supporting their families or investing back home. The measure is part of a sweeping tax bill championed by House Republicans and former President Trump, with the revenue earmarked to offset the cost of extending tax cuts, expanding child tax credits, and bolstering border security.

On paper, the Joint Committee on Taxation estimates this remittance tax could raise about $20 billion over 10 years. But scrutinizing the rationale reveals a disconnect with reality. For one, $2 billion per year is a drop in the bucket of U.S. revenues – potentially achieved at the cost of alienating immigrant communities and U.S. allies. Moreover, this policy effectively targets a narrow group (working immigrants) to pay for broad benefits. It’s a case of “taxation without representation”, critics note, since these non-citizens have no voting power. The Indian diaspora in particular sees it as double taxation: their income was already taxed by the IRS, and now sending post-tax dollars to family would be taxed again. This raises fairness and discrimination concerns, with overseas Indians and policy experts arguing the measure unfairly shifts America’s fiscal burdens onto immigrant shoulders.

Economic behavior is likely to adjust in response, undermining the bill’s goals. Facing extra costs, immigrants may send money less often or look for informal channels. Instead of a monthly $1,000 transfer, a worker might consolidate into quarterly lump sums to cut down fees.

A ₹5,000 Crore Squeeze: Impact on Indian Diaspora Finances

India is the world’s top recipient of remittances, and Indian expatriates in the U.S. are key contributors to that title. In 2023, remittances from the U.S. to India totaled roughly $32–33 billion – about 28% of India’s record-high $118.7 billion inward remittances. This massive flow of funds supports millions of households in India. If the 5% tax is enacted, **Indian families stand to lose $1.6–1.7 billion annually in transferred income, siphoned away to the U.S. Treasury instead of reaching homes in India.

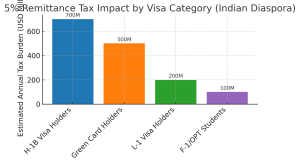

Which groups feel the most pain? Broadly, high-skilled Indian workers on H-1B visas and those freshly on green cards are hit hardest, as they comprise a large share of remitters in the U.S. tech and business sectors. These professionals often send money to support parents, pay mortgages or invest in Indian assets, meaning the 5% cut will be felt on both sides of the ocean. For example, an H-1B engineer sending $1,000 a month to her parents would lose $50 each time – a total of $600 in tax per year. Even Indian students and recent graduates on F-1 visas or OPT are not spared. While they remit less on average, those who, say, send a few hundred dollars occasionally (perhaps from campus jobs or internship earnings) will feel the pinch of a tax that has no minimum threshold. A student wiring $200 home for a birthday gift loses $10 to Uncle Sam – trivial to the U.S. budget but meaningful for a tight student budget.

Conclusion: A Big Bill with Bigger Implications

As advisors in the immigration and global mobility arena, we see “The One Big Beautiful Bill” as a case study in well-intentioned policy colliding with global reality. Yes, funding infrastructure, tax credits, or security is important – but doing so on the backs of immigrant workers could carry unintended consequences far outweighing the modest fiscal gains. The 5% remittance tax, if implemented, would send ripples from rural Kerala to corporate America: families tightening budgets, businesses adjusting compensation for expat staff, and allied nations questioning U.S. goodwill.

From an economic standpoint, the tax represents a small win for the U.S. Treasury (~$2B a year) with a potentially large loss of goodwill. The Indian diaspora has long been a pillar of India-U.S. relations – contributing to both economies, fostering innovation, and acting as informal ambassadors. Squeezing them financially risks eroding trust and dampening the very cross-border exchanges of talent and capital that benefit America in the long run. Geopolitically, it hands critics ammunition to claim the U.S. is adopting a transactional, even discriminatory stance toward immigrants, at a time when strategic partners like India are courted on the global stage.

In the larger picture, the remittance tax saga underscores the need for policymakers to balance economic goals with immigrant realities. A one-size-fits-all excise on remittances may inadvertently harm the very communities that make the U.S. competitive and culturally vibrant. As we continue to advise clients on U.S.-India mobility and strategy, one hope remains: that cooler heads recognize this proposal’s downsides and seek alternatives that don’t undermine a key artery of the global economy. In the end, a truly “big, beautiful” bill would strengthen – not strain – the bridges between America and its immigrant talent, keeping the lifeblood of remittances flowing freely for the benefit of all.

Sources: Reserve Bank of India data on remittance; U.S. House Ways & Means proposal; Business Standard and Times of India coverage of diaspora; Business Today analysis of tax ; National Taxpayers Union ; Travelobiz news